Real estate investment is a dynamic and multifaceted field that offers investors a variety of opportunities to build wealth, generate income, and diversify portfolios. At the core of successful real estate investing lies a need for a deep understanding of the fundamental financial principles and formulas that govern investment decision-making.

From assessing the profitability of income-producing properties to evaluating financing options and analyzing investment returns, real estate investment formulas serve as powerful tools for investors to make informed decisions in a complex and ever-evolving market.

These formulas provide quantitative insights into key aspects of real estate investment, ranging from property valuation and financing to cash flow analysis and return on investment. By leveraging these formulas, investors can assess the financial feasibility and profitability of potential investment opportunities, identify risks and opportunities, and optimize their investment strategies to achieve their financial goals.

In this guide, we will explore some of the most important formulas used in real estate investment, including but not limited to metrics such as Net Operating Income (NOI), Cap Rate, Loan-to-Value Ratio (LTV), Debt Service Coverage Ratio (DSCR), and Internal Rate of Return (IRR). Each of these formulas plays a critical role in evaluating different aspects of real estate investments, providing investors with valuable insights into property performance, financing options, and investment returns.

Whether you're a seasoned real estate investor or just starting out on your investment journey, understanding these formulas is essential for making sound investment decisions and maximizing your success in the real estate market.

1. Loan-to-Value Ratio (LTV)

The Loan-to-Value Ratio (LTV) is a key metric utilized by lenders to gauge the level of risk associated with a loan. It serves as a measure of the relationship between the loan amount and the appraised value or purchase price of the property.

It represents the ratio of the loan amount to the appraised value or purchase price of the property. This ratio is pivotal in determining the terms of a mortgage, encompassing factors such as interest rates, loan eligibility, and the necessity for private mortgage insurance (PMI).

Calculating LTV involves dividing the loan amount by the appraised value or purchase price of the property, then expressing this ratio as a percentage. A lower LTV ratio implies that the borrower has a greater stake or equity in the property, which is typically viewed as less risky by lenders. Conversely, a higher LTV ratio indicates a lesser amount of equity held by the borrower, thereby elevating the lender's risk exposure.

LTV profoundly influences the terms offered by lenders in mortgage transactions. Lenders typically favor lower LTV ratios as they signify reduced risk. Borrowers with higher LTV ratios may encounter higher interest rates, more stringent qualification criteria, or the requirement for private mortgage insurance (PMI) to mitigate the lender's risk of default.

Lenders rely on LTV ratios as a risk management tool. A lower LTV ratio provides a cushion of equity, safeguarding the lender in the event of default. This is particularly significant during periods of declining property values, as borrowers with lower LTV ratios are less susceptible to owing more than the property's worth, a situation known as being "underwater."

LTV ratios find widespread application in mortgage lending for both residential and commercial properties, as well as in refinancing transactions to assess available equity. Overall, understanding and managing LTV ratios are crucial for both borrowers and lenders alike, as they play a pivotal role in shaping the terms of mortgage loans and mitigating risk in real estate transactions. You can read more about LTV in this article where we discuss LTV, ARV, and LTC.

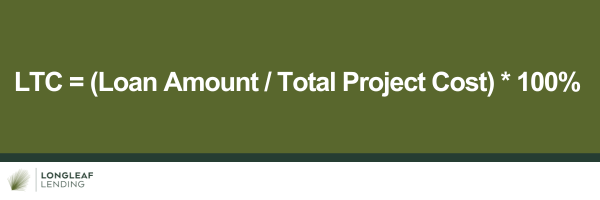

2. Loan-to-Cost Ratio (LTC)

Similar to LTV, LTC is a ratio used in construction and development projects to assess the risk of a loan compared to the total cost of the project. It represents the ratio of the loan amount to the total cost of the project. It evaluates the level of financing relative to the total cost of a project, including both hard and soft costs. LTC helps lenders assess the risk associated with financing a development project and determine the appropriate terms for the loan.

In the formula above, note that Total Project Cost encompasses all expenses associated with the development or construction project, including land acquisition costs, construction costs, permits and fees, design and engineering fees, financing costs, contingency reserves, and any other expenses directly related to the project.

Loan Amount refers to the total amount of financing provided by the lender to fund the development project. The loan may cover a portion of the total project cost, with the developer contributing the remaining portion as equity.

A lower LTC ratio indicates that the developer has a larger equity stake in the project, which is perceived as less risky by lenders. Conversely, a higher LTC ratio suggests that the developer is relying more heavily on debt financing, potentially increasing the lender's risk exposure.

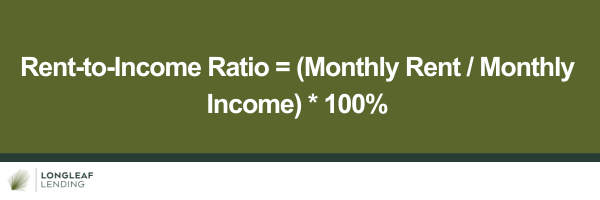

3. Rent-to-Income Ratio

The Rent-to-Income Ratio is a metric used to assess the affordability of rental housing for tenants. It compares the amount of rent paid by a tenant to their monthly income, providing insights into their ability to afford housing expenses. Landlords and property managers also use this ratio to evaluate prospective tenants and ensure that rental payments are reasonable relative to their income.In the formula, Monthly Rent refers to the total amount of rent charged for occupying a rental property on a monthly basis. It includes the base rent as well as any additional charges for utilities, parking, or amenities. Monthly income represents the total monthly income earned by the tenant, typically before taxes and deductions. It includes wages or salary from employment, as well as income from other sources such as investments, government benefits, or rental properties.

The Rent-to-Income Ratio indicates the percentage of a tenant's income that is allocated towards rent. A lower ratio suggests that the rent is more affordable relative to the tenant's income, while a higher ratio indicates that a larger portion of the income is spent on rent, potentially leading to financial strain. While there is no universal standard for an acceptable Rent-to-Income Ratio, many landlords and property managers use thresholds to determine affordability.

For example, a common guideline is that rent should not exceed 30% of a tenant's gross monthly income. However, this threshold may vary depending on factors such as location, market conditions, and tenant preferences.

Landlords and property managers often use the Rent-to-Income Ratio as part of the tenant screening process to assess the financial stability of prospective tenants. A lower ratio indicates that the tenant is more likely to afford the rent without difficulty, while a higher ratio may raise concerns about the tenant's ability to meet their financial obligations.

Property owners may adjust rental rates based on the Rent-to-Income Ratio to ensure that they remain competitive in the market while also maintaining affordability for tenants. This may involve periodic reviews of rental rates in relation to changes in income levels and market conditions.

Rent-to-Income Ratio provides valuable insights into the affordability of rental housing for tenants and is used by both landlords and tenants to assess financial stability and make informed decisions regarding rental agreements. By comparing rent to income, this ratio helps ensure that housing expenses are manageable for tenants and contributes to the overall financial health of both tenants and landlords.

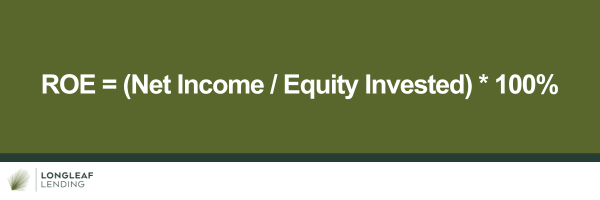

4. Return on Equity (ROE)

Return on Equity (ROE) is used to evaluate the profitability of an investment relative to the equity invested in the investment. ROE measures the return generated from the equity portion of the investment, excluding any debt financing. It provides insights into the efficiency of utilizing equity capital to generate profits from real estate investments.In the formula, Equity Investment represents the amount of capital invested by the investor in the real estate property. Equity can include the initial purchase price of the property, any additional capital invested for improvements or renovations, and the accumulated equity from appreciation over time.

Net Income refers to the total income generated from the real estate investment after deducting all operating expenses, taxes, and other costs associated with property ownership. It includes rental income, proceeds from property sales, and any other sources of income related to the investment.

ROE can be used to compare the performance of different real estate investments or investment strategies. Investors can assess which investments or strategies are more effective in generating returns on equity and allocate capital accordingly. While ROE provides insights into profitability, it's essential to consider the associated risks of real estate investments. Higher returns may come with higher risks, such as vacancy rates, market volatility, or property depreciation.

Investors should assess risk-adjusted returns and consider diversification strategies to mitigate risk.ROE is particularly relevant for long-term investors who aim to build wealth through real estate investments. By maximizing ROE, investors can enhance the growth potential of their equity capital over time and achieve their financial goals.

Investors may use ROE as a benchmark to evaluate whether to retain or divest from existing real estate investments. Properties with lower ROE may be candidates for divestment, allowing investors to redeploy capital into investments with higher return potential.

5. Cap Rate (Capitalization Rate)

The Capitalization Rate (Cap Rate) is a fundamental metric used in real estate investment to evaluate the potential return on an investment property. This measures the rate of return on a real estate investment property based on the income that the property is expected to generate.

It's a ratio that expresses the relationship between a property's net operating income (NOI) and its current market value or purchase price and can be calculated by dividing the property's net operating income (NOI) by its current market value or purchase price.In the formula above, Net Operating Income (NOI) is a key component in calculating the Cap Rate. It represents the total income generated from the property minus all operating expenses. Operating expenses typically include property taxes, insurance, maintenance, utilities, property management fees, and other costs associated with operating the property.

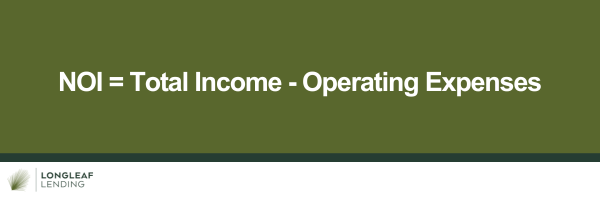

As you will learn in the next item on this list, NOI = Total Income - Operating Expenses.

The Cap Rate compares the NOI to the current market value of the property or its purchase price. This value can be determined by recent comparable sales, appraisals, or market analysis.

A higher Cap Rate indicates a higher potential return on investment, while a lower Cap Rate suggests a lower potential return. However, it's essential to consider other factors such as location, market conditions, property condition, and risk factors when evaluating the significance of the Cap Rate.

Cap Rate is commonly used by investors to compare different investment opportunities and assess their relative attractiveness. It helps investors determine if the property's income potential justifies its current market value or purchase price.

While Cap Rate is a useful tool for initial screening and comparison of investment properties, it has limitations. It doesn't account for financing, taxes, or changes in property value over time. Additionally, it assumes that the property's income and expenses will remain constant, which may not always be the case.

Overall, Cap Rate provides investors with a quick and straightforward way to evaluate the income potential of an investment property relative to its market value or purchase price. However, it should be used in conjunction with other financial metrics and factors to make informed investment decisions.

6. Net Operating Income (NOI)

Net Operating Income is used to evaluate the profitability of income-producing properties. It represents the total income generated from the property minus all operating expenses, excluding debt service and income taxes. NOI provides insight into the property's potential to generate cash flow and is a crucial factor in determining its value and investment potential.While we have briefly touched on NOI in Cap Rate, let’s explain it a bit further below.

In the formula, Total Income refers to all revenue generated from the property, including rental income from tenants, parking fees, vending machine income, laundry income, and any other sources of revenue directly related to the property.

Operating Expenses encompass all costs associated with operating and maintaining the property. This includes property taxes, insurance premiums, property management fees, utilities (such as water, electricity, and gas), maintenance and repairs, landscaping, janitorial services, HOA fees (if applicable), and any other recurring expenses necessary to keep the property operational.

Take note that NOI excludes certain expenses such as debt service (mortgage payments), capital expenditures (major property improvements or upgrades), depreciation, and income taxes. By excluding these expenses, NOI provides a clearer picture of the property's operational performance and cash flow potential.

NOI is a critical metric in real estate investment analysis as it serves as the basis for determining the property's value and potential return on investment. It provides investors with a clear understanding of the property's income-generating potential and its ability to cover operating expenses and generate positive cash flow.

NOI is also used to measure the operational performance of income-producing properties over time. By tracking changes in NOI, investors can assess the property's financial health, identify trends, and make informed decisions regarding property management, leasing strategies, and capital improvements.

NOI provides insights into the property's ability to generate stable and predictable income streams, which is crucial for assessing investment risk. Properties with higher NOI relative to their operating expenses are generally considered less risky investments, as they have greater income stability and cash flow potential.

7. Cash-on-Cash Return

Cash-on-Cash Return is a financial metric used in real estate investment to evaluate the annual return generated on the actual cash invested in a property. It measures the cash flow generated by the property relative to the initial cash investment, providing insight into the profitability of the investment.In relation to the above formula, here are some things to consider:

Total Cash Investment represents the total amount of cash invested by the investor in the property at the time of acquisition. It includes the down payment, closing costs, and any other upfront expenses associated with purchasing the property.

Annual Cash Flow refers to the net income generated from the property on an annual basis after deducting all operating expenses, mortgage payments, property taxes, insurance, maintenance costs, property management fees, and other expenses related to property ownership.

Cash-on-Cash Return measures the annual return generated on the actual cash invested in the property. A higher Cash-on-Cash Return indicates that the property is generating greater cash flow relative to the initial investment, resulting in a higher return on investment. Conversely, a lower Cash-on-Cash Return suggests that the property may be less profitable or efficient in generating cash flow.

While Cash-on-Cash Return provides insights into the annual return on investment, it's essential to consider the associated risks of real estate investments. Higher returns may come with higher risks, such as vacancy rates, market volatility, or property depreciation. Investors should assess risk-adjusted returns and consider diversification strategies to mitigate risk.

8. Gross Rent Multiplier (GRM)

The Gross Rent Multiplier (GRM) is a simple yet valuable financial metric used in real estate investment to evaluate the value of income-producing properties. It measures the relationship between the property's sale price and its gross rental income, providing investors with a quick and straightforward way to assess the investment potential of rental properties.In the formula, Gross Rental Income represents the total annual rental income generated by the property before deducting any operating expenses, vacancies, or other costs associated with property ownership. It includes the total rent collected from all units or spaces within the property. The Sale Price is the total amount paid by the buyer to acquire the property. It includes the purchase price of the property, closing costs, and any other expenses related to the acquisition.

A lower GRM indicates that the property is priced more attractively relative to its rental income, suggesting that it may represent a better investment opportunity. Conversely, a higher GRM suggests that the property may be overpriced relative to its rental income, potentially indicating lower investment potential.

GRM can be used to compare the relative value of different income-producing properties within the same market or across different markets. Investors can assess which properties offer better value based on their rental income relative to their sale price. Changes in GRM over time can provide insights into market trends and investment opportunities. A decreasing GRM may indicate increasing property values or rental income, while an increasing GRM may suggest declining property values or rental income.

While GRM provides a quick and simple way to assess the value of income-producing properties, it has limitations. It does not account for operating expenses, vacancies, financing costs, or other factors that may affect the property's profitability. Therefore, investors should use GRM in conjunction with other financial metrics and factors to make informed investment decisions.

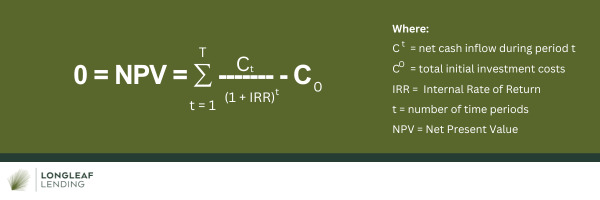

9. Internal Rate of Return (IRR)

Internal Rate of Return (IRR) is used to evaluate the profitability of an investment over time. In real estate, IRR measures the annualized rate of return that an investor can expect to receive from a property investment, taking into account the timing and magnitude of cash flows, including both income and expenses.

IRR is calculated by solving for the discount rate that equates the present value of all cash inflows with the present value of all cash outflows. In other words, IRR is the discount rate that makes the net present value (NPV) of the investment equal to zero.Mathematically, IRR is found by setting the equation:IRR is then determined iteratively using numerical methods or financial calculators/software.

A higher IRR indicates a more attractive investment opportunity, as it represents a higher rate of return relative to the initial investment. Conversely, a lower IRR suggests a less favorable investment opportunity.

IRR is sensitive to changes in cash flow assumptions, such as rental income, operating expenses, property appreciation, and financing terms. Investors should conduct sensitivity analysis to assess how variations in these factors affect the IRR and the overall investment viability.

While IRR provides valuable insights into investment returns, it has limitations. IRR assumes reinvestment of cash flows at the same rate of return, which may not always be realistic. Additionally, IRR may produce multiple solutions (e.g., in the case of non-conventional cash flow patterns), requiring careful interpretation and consideration of other factors.

10. Debt Service Coverage Ratio (DSCR)

Debt Service Coverage Ratio (DSCR) is another financial metric used by lenders and investors to assess the ability of an income-producing property to generate sufficient cash flow to cover its debt obligations, particularly mortgage payments.

It provides insight into the property's ability to generate income to meet its debt service requirements and is an essential factor in determining the property's financing terms and investment viability.Read more about DSCR here and discover our DSCR loans.

Longleaf Lending offers an array of hard money loan programs for real estate investors. Visit our Loan Products page to learn more on how we can serve you in your real estate investment projects.

Instantly evaluate your next project

Use our real estate loan calculator and assess your next project - it only takes 30 seconds.